Lowering monthly expenses does not have to mean giving up comfort or fun. Many people think saving money requires extreme cuts, but small and steady changes can make a big difference. By adjusting daily habits, reviewing regular bills, and making smarter choices, it is possible to free up cash while still enjoying a comfortable life. This article explores practical and realistic ways to reduce monthly costs without feeling deprived.

Understanding Where Your Money Goes

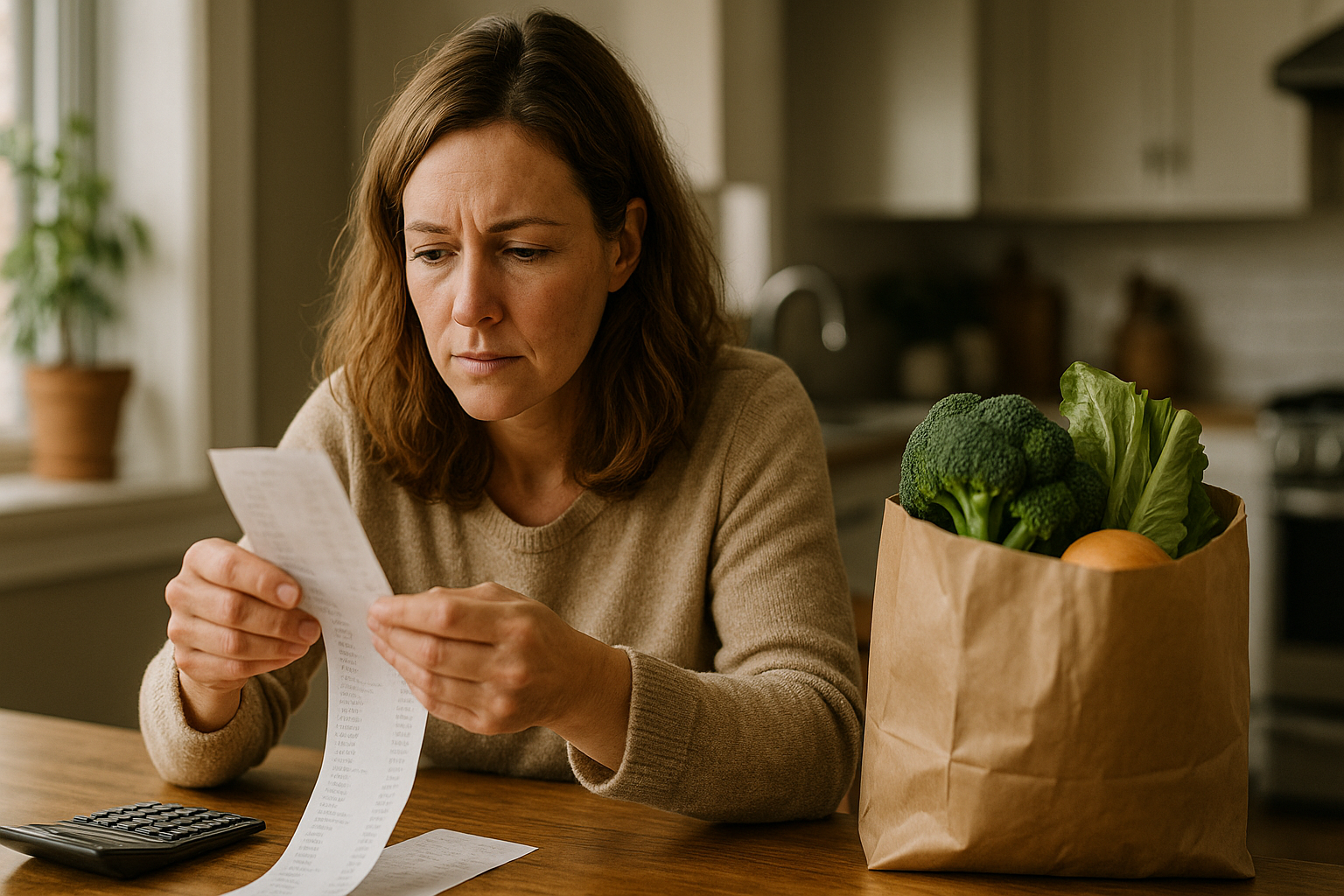

Before making changes, it helps to understand current spending. Many expenses feel small on their own but add up over time. A clear picture of spending makes it easier to find areas to adjust.

Track Monthly Spending

Tracking expenses for at least one month can reveal patterns. This includes fixed bills and daily spending. Writing things down or using an app helps show where money actually goes, not where you think it goes.

- List all fixed costs like rent, insurance, and phone plans.

- Track daily spending such as food, coffee, and entertainment.

- Review bank and credit card statements for missed items.

Separate Needs from Wants

Needs are essentials like housing, utilities, food, and transportation. Wants are extras like dining out, subscriptions, and impulse purchases. Knowing the difference helps guide better decisions without cutting essentials.

Lowering Housing Costs

Housing is often the largest monthly expense. Small adjustments can reduce costs without changing where you live.

Review Rent or Mortgage Options

If renting, it may be possible to negotiate at lease renewal, especially with a good payment history. For homeowners, refinancing could lower monthly payments if interest rates are favorable.

- Ask landlords about lease renewal discounts.

- Compare mortgage rates every few years.

- Consider longer loan terms if cash flow is tight.

Reduce Utility Usage at Home

Utilities can quietly drain money. Simple habits can reduce bills without affecting comfort.

- Turn off lights and electronics when not in use.

- Use energy-efficient bulbs and appliances.

- Adjust thermostat settings slightly during sleep or work hours.

Cutting Utility and Service Bills

Monthly service bills are often negotiable or adjustable with little effort.

Internet and Cable Services

Many households pay for more speed or channels than needed. Reviewing plans once a year can uncover savings.

- Call providers and ask about promotions.

- Remove unused premium channels.

- Consider streaming services instead of cable.

Mobile Phone Plans

Phone plans often include features that go unused. Switching plans or providers can reduce costs.

- Choose plans based on actual data usage.

- Look into family or group plans.

- Consider prepaid or smaller carriers.

Saving Money on Food

Food is a daily expense that offers many chances to save without eating poorly.

Plan Meals Ahead

Meal planning helps reduce waste and impulse purchases. Planning a week at a time is often enough.

- Create a shopping list before going to the store.

- Plan meals around sales and seasonal foods.

- Cook larger portions and save leftovers.

Grocery Shopping Smarter

Small changes in shopping habits can lower grocery bills significantly.

- Buy store brands instead of name brands.

- Avoid shopping when hungry.

- Use loyalty programs and digital coupons.

Reduce Dining Out Costs

Eating out is enjoyable, but it can be expensive. Cutting back does not mean cutting it out completely.

- Limit dining out to special occasions.

- Choose lunch specials instead of dinner.

- Cook favorite restaurant meals at home.

Transportation Savings

Transportation costs include fuel, maintenance, insurance, and public transit. Reviewing these areas can uncover savings.

Reduce Fuel and Maintenance Costs

Driving habits and vehicle care play a big role in costs.

- Keep tires properly inflated.

- Combine errands to reduce trips.

- Follow regular maintenance schedules.

Consider Alternative Transportation

Depending on location, alternatives to driving can lower expenses.

- Use public transportation when possible.

- Carpool with coworkers or friends.

- Walk or bike for short trips.

Managing Insurance Costs

Insurance is necessary, but overpaying is common. Reviewing policies regularly can lead to savings.

Shop Around for Better Rates

Insurance companies change rates often. Comparing quotes every year or two helps keep costs low.

- Compare auto and home insurance annually.

- Ask about discounts for bundling policies.

- Maintain a good credit score for better rates.

Adjust Coverage Carefully

Coverage should match current needs. Paying for unnecessary coverage increases monthly costs.

- Review deductibles and coverage limits.

- Remove add-ons that no longer apply.

- Reassess life insurance after major life changes.

Controlling Subscription Spending

Subscriptions are easy to forget but can add up quickly.

Audit Monthly Subscriptions

Many people pay for services they rarely use.

- List all streaming, apps, and memberships.

- Cancel services used less than once a month.

- Share family plans when allowed.

Rotate Entertainment Services

Instead of paying for multiple services at once, rotate them throughout the year.

- Subscribe to one service at a time.

- Cancel after finishing favorite shows.

- Restart later if needed.

Reducing Debt Payments

Debt can take a large part of monthly income. Managing it wisely frees up cash.

Refinance or Consolidate Debt

Lower interest rates can reduce monthly payments.

- Look into refinancing high-interest loans.

- Consider consolidation for multiple debts.

- Avoid extending debt for unnecessary purchases.

Pay More Than the Minimum When Possible

Paying extra reduces interest over time, which lowers future expenses.

- Apply extra money to the highest interest debt.

- Use windfalls like tax refunds wisely.

- Set up automatic extra payments if possible.

Smarter Shopping Habits

Shopping choices affect monthly budgets more than many realize.

Wait Before Big Purchases

Giving yourself time reduces impulse buying.

- Wait 24 to 48 hours before non-essential purchases.

- Research prices and read reviews.

- Look for sales or open-box options.

Buy Used or Borrow When Possible

Used items can offer the same value at a lower price.

- Shop secondhand stores or online marketplaces.

- Borrow tools or equipment used rarely.

- Sell unused items to offset costs.

Healthcare and Wellness Savings

Health-related expenses are important but can often be managed better.

Use Preventive Care

Preventive care helps avoid costly treatments later.

- Schedule annual checkups covered by insurance.

- Use in-network providers.

- Ask about generic medications.

Compare Medical Costs

Prices can vary widely for the same service.

- Ask for cost estimates before procedures.

- Use health savings accounts if available.

- Review medical bills for errors.

Affordable Entertainment and Fun

Enjoying life does not require high spending.

Explore Free and Low-Cost Activities

Many communities offer affordable entertainment options.

- Visit parks, libraries, and community events.

- Attend free workshops or classes.

- Host game or movie nights at home.

Set a Fun Budget

Planning entertainment spending helps avoid overspending.

- Decide on a monthly fun amount.

- Choose activities that bring the most joy.

- Track spending to stay within limits.

Family and Household Savings

Households with families have unique opportunities to save.

Buy in Bulk for Regular Items

Bulk buying can reduce the cost per unit.

- Stock up on non-perishable items.

- Share bulk purchases with others.

- Avoid bulk buying items that may go to waste.

Hand-Me-Downs and Swaps

Children outgrow items quickly, making swaps practical.

- Trade clothes and toys with friends.

- Use community swap groups.

- Donate and receive items as needed.

Banking and Financial Service Fees

Fees can quietly reduce available cash each month.

Choose Low-Fee Accounts

Many banks offer no-fee checking and savings accounts.

- Review bank statements for monthly fees.

- Switch to online banks with lower costs.

- Meet minimum balance requirements when possible.

Avoid Unnecessary Charges

Small charges add up over time.

- Set up account alerts to avoid overdrafts.

- Use in-network ATMs.

- Pay bills on time to avoid late fees.

Tax and Work-Related Savings

Work and tax decisions affect take-home pay.

Adjust Tax Withholding

Proper withholding ensures more money in each paycheck.

- Review withholding after life changes.

- Avoid large refunds caused by over-withholding.

- Use employer tools to estimate taxes.

Take Advantage of Employer Benefits

Benefits can reduce out-of-pocket costs.

- Use flexible spending or health accounts.

- Join commuter benefit programs.

- Participate in wellness incentives.

Building Better Money Habits

Long-term savings often come from mindset shifts.

Set Clear Financial Goals

Goals give purpose to saving and spending choices.

- Define short-term and long-term goals.

- Track progress monthly.

- Celebrate milestones in low-cost ways.

Practice Mindful Spending

Being aware of spending decisions reduces regret.

- Ask if purchases add real value.

- Focus on experiences over things.

- Review spending regularly to stay aware.